The S&P closed Friday at a fresh high, up 9.8% on the month. On Wednesday and Thursday, five companies that together represent roughly a quarter of the S&P 500's market cap will report earnings: Microsoft, Meta, Alphabet, Amazon, and Apple.

We look to deploy cash after earnings. The rationale is not that earnings will be bad, it's that the earnings vs. stock movement symmetry has shifted.

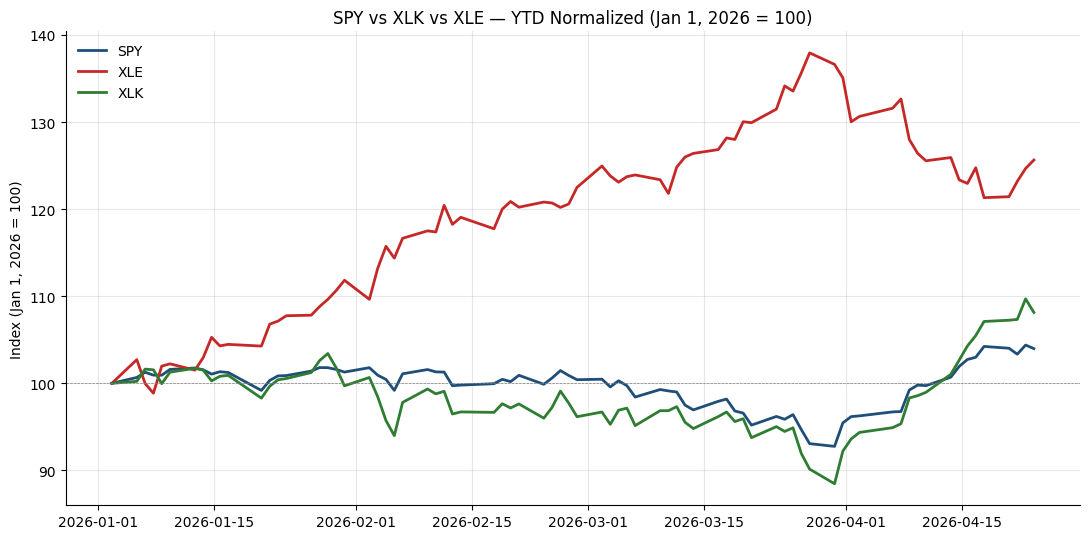

Energy is leading the index because of the Iran-driven crude bid, but Tech caught up in April. The setup that produced both — concentration in five names plus an unresolved geopolitical premium — is what gets tested this week.

| Ticker | Last | April % | YTD % | Earnings Date |

|---|---|---|---|---|

| AMZN | $255.08 | +21.14% | +12.62% | Thu, Apr 30 |

| GOOGL | $338.89 | +13.95% | +7.61% | Wed, Apr 29 |

| META | $659.15 | +13.80% | +1.43% | Wed, Apr 29 |

| NVDA | $199.64 | +13.59% | +5.72% | Wed, May 20 |

| MSFT | $415.75 | +12.56% | -11.89% | Wed, Apr 29 |

| SPY | $708.45 | +8.12% | +3.98% | -- |

| AAPL | $273.43 | +6.96% | +0.99% | Thu, Apr 30 |

| TSLA | $373.72 | -1.98% | -14.69% | Out: Apr 22 |

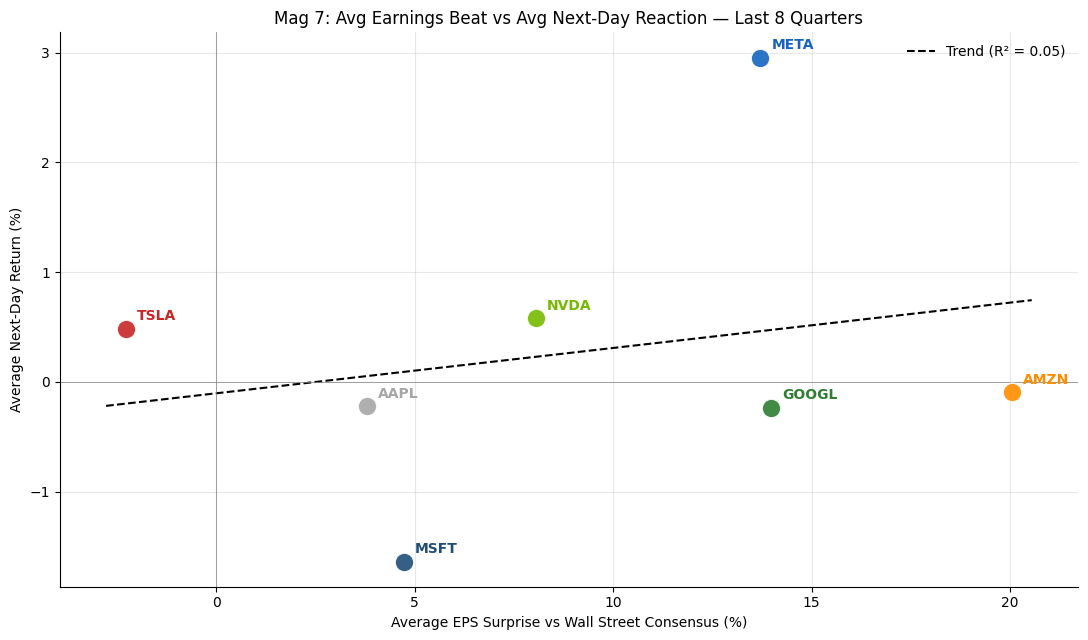

As studied before, the market has stopped paying for beats:

Microsoft beats Wall Street consensus by an average of 4.7% and the stock falls 1.6% the next day. Amazon beats by 20% and moves -0.1% — essentially nothing. Alphabet beats by 14% and goes nowhere. The R² across the seven names is 0.05. Beat size and next-day reaction have decoupled.

Three of the five names reporting this week — Microsoft, Amazon, Alphabet — sit in the lower-right of the chart. Large beats, neutral-to-negative reactions. The market is no longer pricing earnings alone. It is pricing the guidance, the capex framing, and the monetization detail. Meta is the lone positive outlier, but its yet to recover from a bad Q3 earnings call.

On energy:

WTI sits near $96.50, Brent above $105. The consensus narrative — that the ceasefire holds and crude mean-reverts to the mid-$70s — is being priced as if the deal is already done. It is not. The Iranian parliament's chief negotiator resigned from talks Thursday. We are holding XLE exposure into the fragility window. The invalidation is a confirmed deal with verified compliance and crude back below $80.

The central banks are the underwatched risk:

Four meetings this week: BoJ Tuesday, Fed Wednesday, ECB and BoE Thursday. The Fed, ECB, and BoE are expected to hold and the market has priced it that way. The BoJ is where the asymmetry sits.

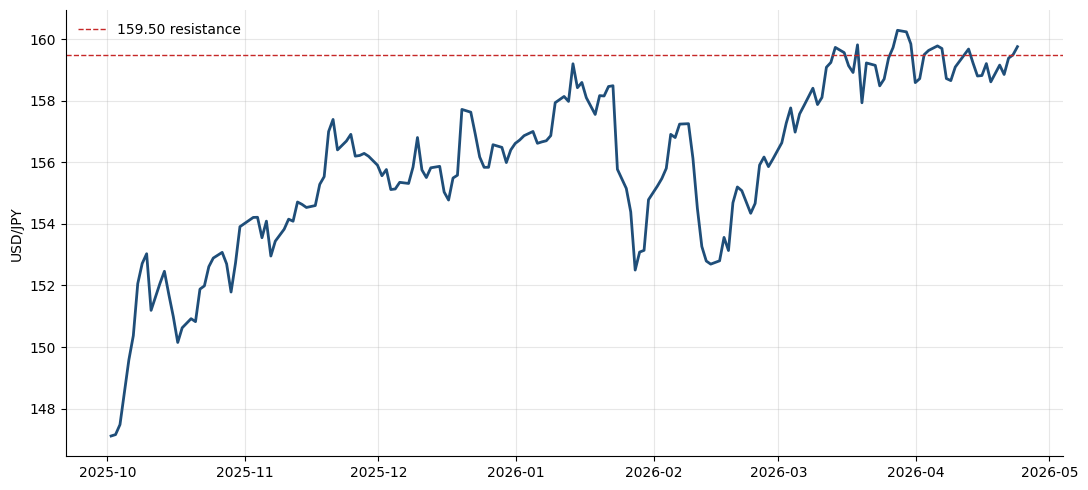

USD/JPY has tested 159.50 repeatedly over the past six weeks without breaking. The market is pricing the possibility of up to 50bps of hikes from the BoJ before year-end, but a hawkish surprise on Tuesday is the cleanest path to a global carry-trade unwind — the same mechanism that drove the August 2024 volatility event. Most US-focused portfolios are not hedged for it.

Bottom line:

The Mag 7 print into elevated expectations after a 9.8% monthly rally with capex pressure compounding. The downside scenario produces a multi-day drawdown the market has been rehearsing for two years. Trimming tech and raising cash is the trade.

You don't pay for asymmetry by waiting for the catalyst. You pay for it by being early.

This positioning is implemented selectively for clients within our Core allocation strategy and the HBM & AI Infrastructure tactical sleeve, based on individual objectives and risk tolerance. Not all clients are invested in this strategy.