For 40 days, the Iran war compressed everything. Equities sold off indiscriminately. Oil spiked from $67 to $112 a barrel. The VIX ran. Institutional capital rotated toward energy and defense, away from growth and technology. Markets did what they always do in a genuine shock: they stopped distinguishing between companies whose fundamentals changed and companies that simply happened to be in the risk-off blast radius.

Wednesday's ceasefire — a two-week pause brokered by Pakistan, fragile by every measurable indicator — triggered a relief rally. The Dow added 1,325 points. The S&P 500 gained 2.5%. Oil dropped 18% in a single session. The market exhaled.

The war didn't change the AI infrastructure buildout by a single dollar. The ceasefire doesn't change it either. What both events did was create a pricing dislocation we intend to use.

If peace holds, markets normalize and capital rotates back into growth and AI infrastructure — the sleeve re-rates. If it doesn't, we get more entry opportunity in names we already have high conviction in at cheaper prices. Either way, the AI infrastructure buildout doesn't stop. The hyperscaler CapEx doesn't reverse. The thesis is the same on both sides of the outcome.

The MWA HBM and AI Infrastructure Tactical Sleeve holds nine positions built around a single structural thesis: every dollar of hyperscaler capital expenditure — Google, Microsoft, Amazon, Meta — flows through a specific set of memory, optical interconnect, storage, and semiconductor equipment companies before it reaches the income statements of the headline AI names. That CapEx cycle doesn't pause for geopolitical events. Microsoft didn't cancel its GPU cluster buildout because the Strait of Hormuz closed. Google didn't defer its TPU production ramp because oil hit $112. This sleeve is implemented selectively for clients who have elected to participate based on their individual objectives and risk tolerance. Not all clients are invested in this strategy.

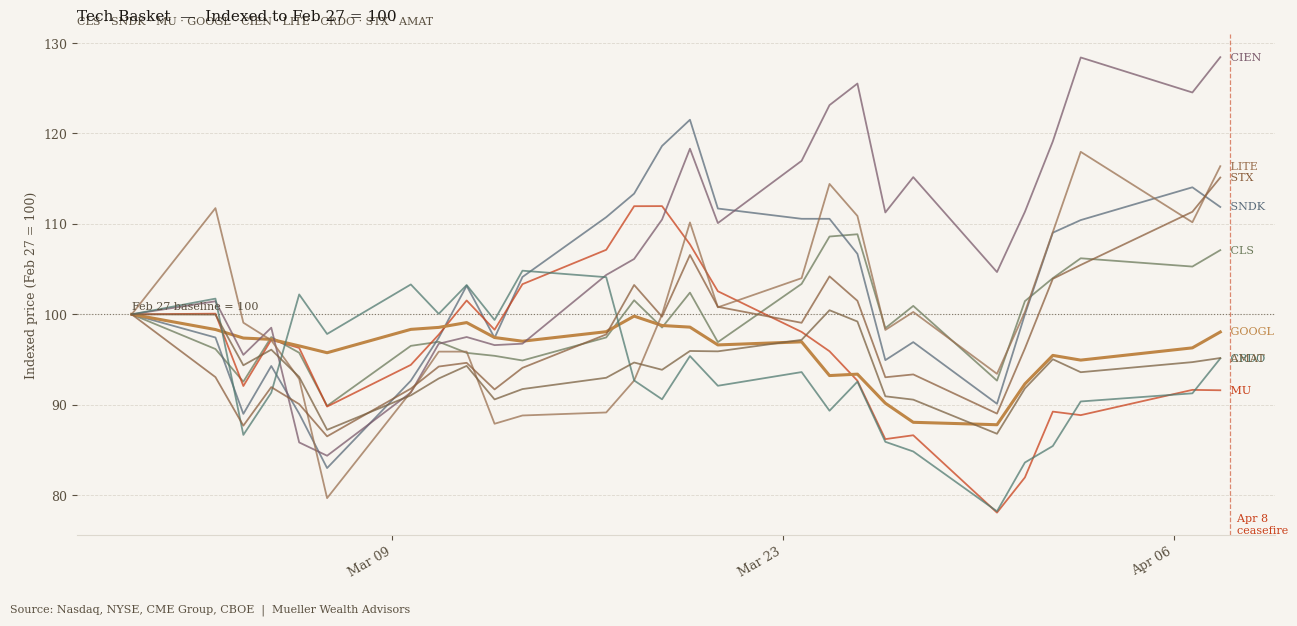

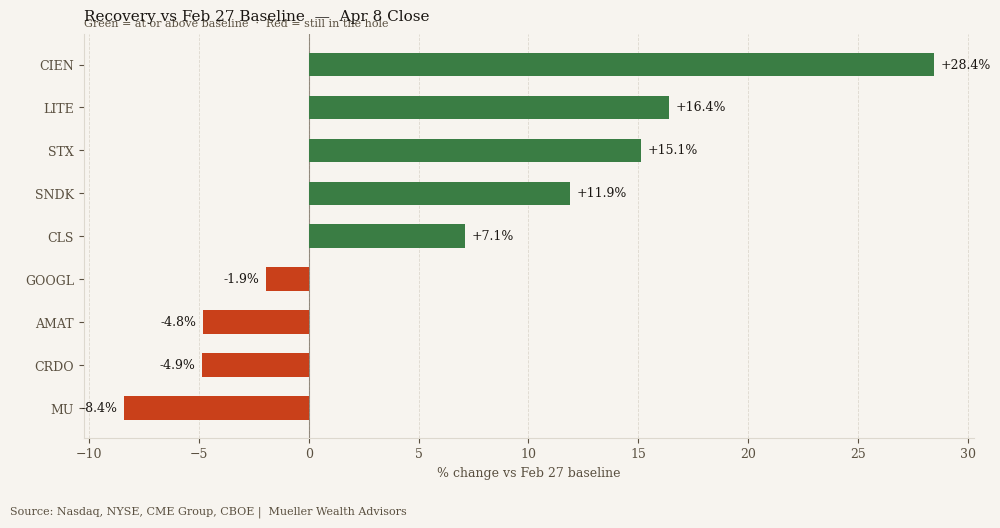

Looking at sleeve performance indexed to the February 27 baseline — the day before Operation Epic Fury began — the data tells a precise story about what the market understood and what it missed. The optical and storage names ran. CIEN is up 28.4% against that baseline as of Wednesday's close. LITE is up 16.4%. STX is up 15.1%. These names benefited from a war-specific demand signal: bandwidth rerouting, data infrastructure urgency, shipping disruption accelerating domestic storage demand. The market correctly bid them up.

The semiconductor and hyperscaler names did not move the same way. GOOGL is down 1.9% against the February 27 baseline as of Wednesday's close. AMAT is down 4.8%. CRDO is down 4.9%. MU is down 8.4%. These are not companies whose business models deteriorated during the conflict. Credo Technology reported Q3 fiscal 2026 revenue of $407 million during the war — a 52% sequential increase and 201% year-over-year growth, pre-announcing $60 million above Street consensus. Micron sits at the center of the HBM supercycle, supplying the high-bandwidth memory every next-generation GPU cluster requires. Applied Materials is one layer back — the equipment that manufactures the chips that build the infrastructure. Their prices did not reflect their execution.

The divergence is not fundamental. It is rotational. But a full rotation is self-correcting by definition — capital displaced by a geopolitical shock returns to where the structural growth is. We are in the early years of an AI infrastructure buildout that will define the next decade of capital expenditure. The money comes back.

Google guided $175 to $185 billion in 2026 capital expenditure — nearly double 2025 levels — with a $240 billion Cloud backlog that doubled year-over-year. Microsoft, Amazon, and Meta have made no revisions to their infrastructure spend. When institutional money rotated out of the laggard group, it wasn't an assessment of fundamentals. It was a mechanical response to uncertainty — portfolio managers reducing beta exposure during a genuine macro shock. The thesis didn't break. The macro got loud. The buildout that drives demand for HBM, interconnect, storage, and fab equipment is accelerating into H2 2026, which is precisely when the revenue inflection hits the income statements of the names in this sleeve.

We are in the infrastructure phase of the AI buildout. The headline names get the attention. This sleeve owns the layer beneath them.

Within the sleeve, we are constructive and incrementally increasing exposure to the names that remain below their pre-war baseline. The setup appears favorable: the macro overhang is lifting, the fundamental trajectory is intact, and the names with the most catch-up potential are the ones most directly exposed to the H2 2026 CapEx inflection.

What the last 40 days clarified is not a new thesis. It confirmed the existing one. The companies building the connective tissue of AI infrastructure kept executing while the macro ran. The market mispriced that execution. The ceasefire is removing the fog, and what's visible underneath is exactly what we expected: a CapEx supercycle with H2 2026 as the revenue inflection point, and four names in this sleeve that haven't been given credit for it yet.

The Iran pause is not the story. The pause in the sleeve's repricing is the opportunity.