When Iran shut down traffic on February 28th, it struck Western energy interests. The IEA called what followed the worst energy disruption in history — more severe than the 1970s oil crises combined. As of April 9th, 230 loaded oil tankers sat trapped inside the Gulf. USO has returned 84% in 90 days. OVX — the crude oil volatility index — sits at 78, more than double its long-run average of 36. But Iran's strategy was shortsighted in a way that is only now becoming clear. By closing the strait, Tehran put its own largest customer, China, directly in the crosshairs — and created the precise conditions that invited a U.S. blockade. What is unfolding now is a once-in-a-generation geopolitical maneuver — precise, patient, and decades in the making. Every shale well drilled, every LNG terminal permitted, every percentage point of import dependence shed was a brick in a wall Washington just finished building. Iran walked straight into it.

The United States imports roughly 8% of its crude from Gulf states. China imports 40% of its crude and 30% of its LNG through that same strait — and imported 1.5 billion barrels of Gulf crude in 2025 alone, with Iranian oil adding another 11% on top. Washington didn't close the strait to hurt Iran. It closed it to make Iran's closure hurt China. That asymmetry was never an accident.

The U.S. doesn't need to defeat Iran militarily. It needs China to do the diplomatic work. The blockade is the mechanism that makes that happen.

China feels every day of this in its industrial cost base, its manufacturing margins, its current account, and its political calculus. Russia and overland pipelines provide a partial buffer. Strategic reserves buy months, not quarters. The longer the strait stays closed, the louder Beijing's internal pressure to resolve it becomes. That is precisely the mechanism Washington designed.

The equity market has not fully processed this. That is the single most important data point in this analysis. The VIX — the market's fear gauge for equities — closed April 13th at 19.23, roughly in line with its 90-day average of 19.83. Calm. Meanwhile OVX, the crude oil volatility index, sits at 78.01 against a 90-day average of 61.99. The oil market is pricing a genuine crisis. The equity market is pricing a manageable disruption. That gap — 19 on VIX versus 78 on OVX — is the detachment. It has closed before. It always closes. The question is which market moves toward the other.

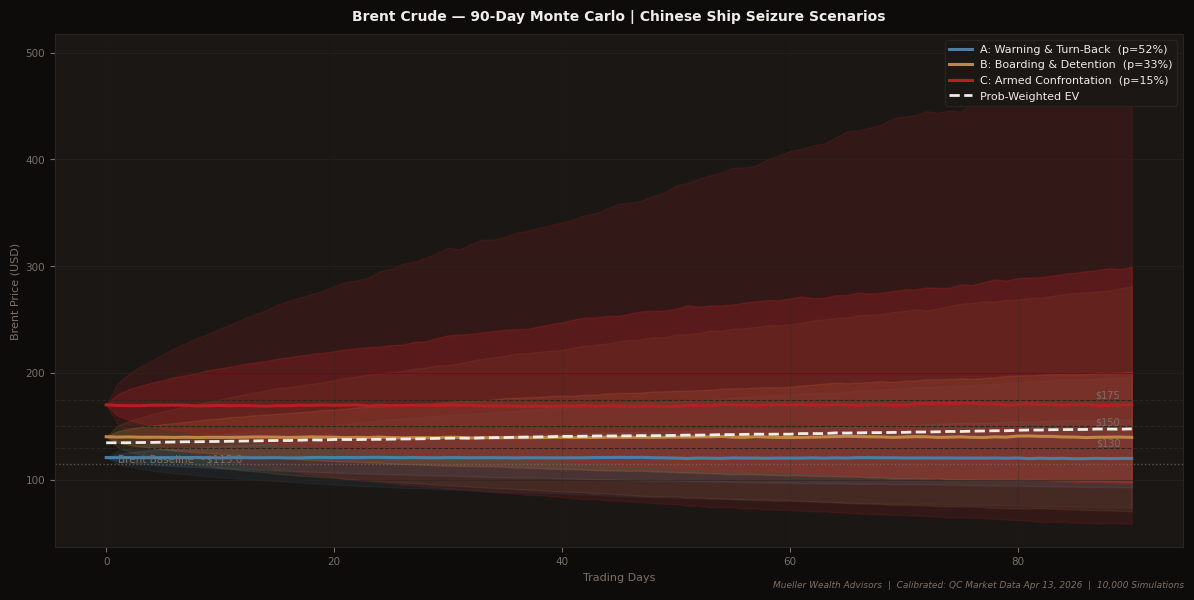

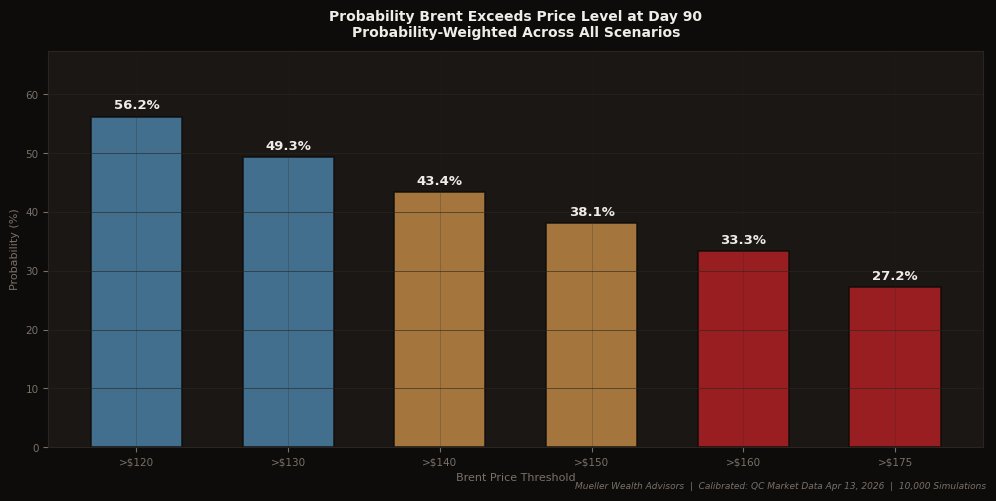

We ran 10,000 Monte Carlo simulations across three scenarios, calibrated to realized market volatility as of April 13th.

Specifically, these model what would happen if a Chinese vessel attempted to cross the blockade — and how markets would respond depending on how that confrontation resolves. Assume the USO annualized vol at 56%, OVX at 78, Brent implied near $115.

A Chinese vessel is intercepted, turns back, Beijing protests diplomatically, state media runs hot for 72 hours. Oil spikes 5% intraday and fades. Equity markets shrug. This is the base case and it is consistent with how these confrontations have historically resolved at the tactical level.

A COSCO or Sinopec-flagged vessel is boarded under U.S. sanctions enforcement authority. This is where the energy crisis and the trade war merge into a single event. Brent reaches $140. Equity markets reprice the geopolitical reality they have been ignoring. The VIX/OVX gap closes — violently and from the wrong direction.

A Chinese naval escort accompanies a tanker and a kinetic incident occurs. Brent reaches $170. The S&P reprices 14% lower. This is not the base case. It is the tail that responsible capital management requires acknowledging.

The scenarios are not predictions. They are a structured way of thinking about the range of outcomes and their relative likelihood.

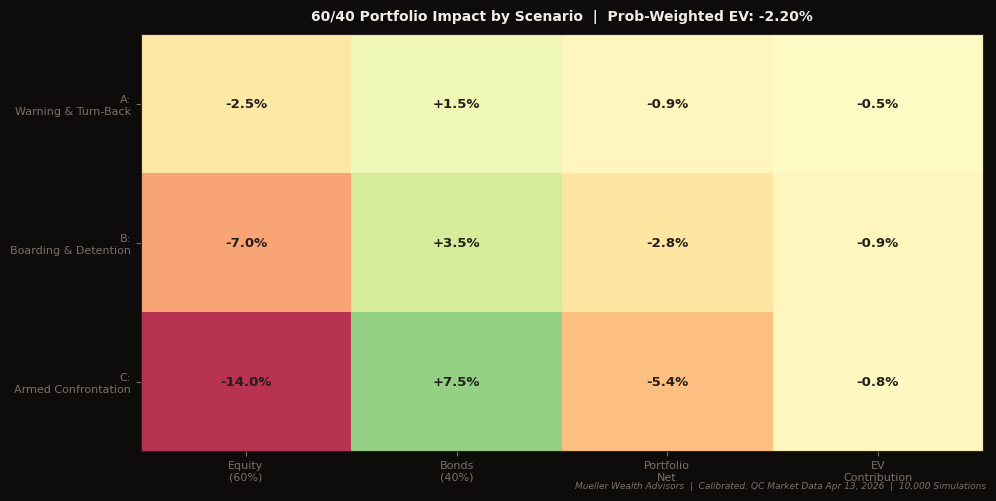

The probability-weighted expected value on a standard 60/40 portfolio across all three scenarios is -1.24%. That is not a catastrophic number in isolation. But it sits on top of an equity market that is already richly valued, a Fed in transition, and a geopolitical environment that has produced more surprises in the past 90 days than the prior three years combined. The -1.24% is the expected hit. The distribution around it is what demands attention.

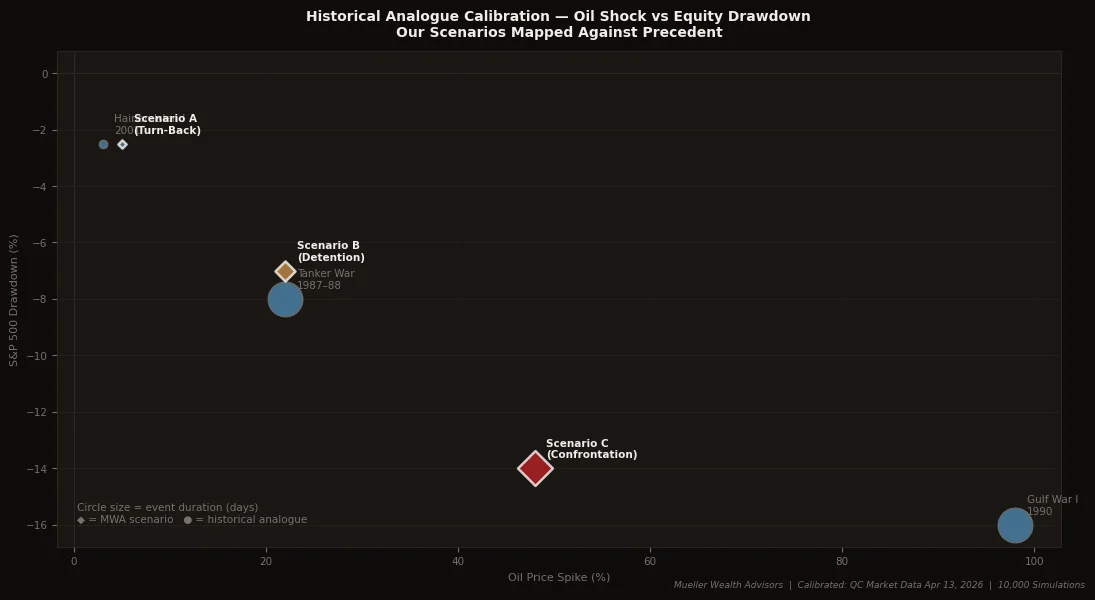

The historical record is instructive. The Hainan Island incident in 2001 — the closest modern analogue to a direct U.S.-China military confrontation — lasted 11 days and produced a 3% oil spike and a 2.5% equity drawdown before resolution. The Tanker War of 1987-88 took 180 days and produced a 22% oil spike. Gulf War I produced a 98% oil spike before markets recovered. In every case, the disruption was finite. In every case, the underlying economic logic eventually reasserted itself.

The invalidation for the asymmetric thesis is specific. It is not military escalation — the probability math already accounts for that. The real invalidation is if China decides that confronting the U.S. economically is preferable to pressuring Iran diplomatically. Rare earth export restrictions, acceleration of yuan internationalization, signaling on U.S. Treasury holdings — these are the instruments of Chinese retaliation that do not require naval engagement and that carry their own cascade risk through global credit markets. That scenario is not the base case. It is the scenario that bears watching.

What most commentary is missing is how Beijing is managing the domestic pain — and what that management costs. China's consumers saw only an 11% increase at the pump while global diesel surged 25%. That gap didn't disappear. It was absorbed by CNPC, Sinopec, and CNOOC — state-owned giants directed by the NDRC to sell refined product below cost regardless of margin. The state covers those losses through directed lending from banks already carrying unresolved property sector NPLs from the 2021-2024 downturn.

When crude exceeds $130 — a level our Monte Carlo puts at 24% probability — domestic fuel prices are frozen entirely by statute. Every barrel processed becomes a loss-making transaction for China.

Those losses don't disappear. They move from the pump to the sovereign balance sheet, accumulating as contingent liabilities that won't surface until an SOE debt restructuring forces the reckoning.

The yuan pressure follows directly. China's current account surplus — historically the anchor of yuan stability — narrows materially when import costs surge at this scale. The People's Bank of China faces a binary choice: defend the peg by burning FX reserves, or allow depreciation and risk capital flight. Neither is clean. The yuan's stability right now is a policy artifact. The structural pressure underneath it compounds every day the strait stays closed.

The contrast with the U.S. could not be more different. American shale producers are generating an estimated $63 billion in additional revenues at $100 oil. The dollar is strengthening — every country scrambling to buy expensive crude must buy dollars first, validating the petrodollar system in the most dramatic fashion in 50 years. The U.S. consumer feels it at the pump. But none of it requires Washington to borrow against its sovereign balance sheet to suppress a price signal it cannot afford its population to see. One country is paying for this crisis at the pump. The other is paying for it in ways that won't appear in any headline for years.

Twenty years of drilling and permitting was never just energy policy. It was preparation for exactly this moment.

Iran thought it was weaponizing the strait against the West. It handed Washington the most elegant economic lever against China in recent times.